Can You Buy Bonds on Wealthsimple in 2024? [Quick Answer]

If you’re someone who knows a little bit about investing and money, you’ve likely heard of “bonds” before. But if you haven’t, a bond is basically just debt security, where the issuer borrows money from investors and promises to repay at maturity.

But the thing with bonds is it’s often hard to know where or how to buy them, which leads to a common question often asked by Wealthsimple users – can you buy bonds on Wealthsimple?

Here’s a quick answer to this question:

No, you can’t directly buy bonds on Wealthsimple. However, you can invest in bond-focused ETFs available on the platform, which offer very similar benefits.

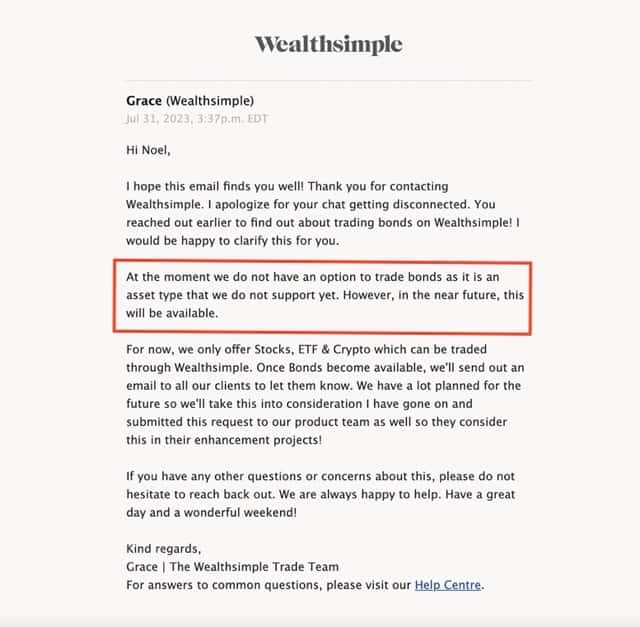

Don’t just take my word for it, though, I contacted Wealthsimple and asked them about this. Here’s what Grace, my customer support rep said.

Now we will break down what this means in the next section, but just know that you can get exposure to bonds with Wealthsimple, but only through ETFs, not by owning the bonds directly.

Can I Invest in Bonds with Wealthsimple?

So as just mentioned, you can’t directly buy bonds on Wealthsimple, but you can buy into bond ETFs on either the Wealthsimple Trade or Invest platform, which is very similar to owning the bond itself.

What are Bond ETFs?

Bond ETFs [1] are a specific category of exchange-traded funds that solely invest in bonds. They mirror the concept of bond mutual funds, maintaining a diverse portfolio of bonds guided by distinct strategies—ranging from U.S. Treasuries to high-yield bonds—and varying holding durations, from short to long-term.

Buying Bond ETFs on Wealthsimple Trade

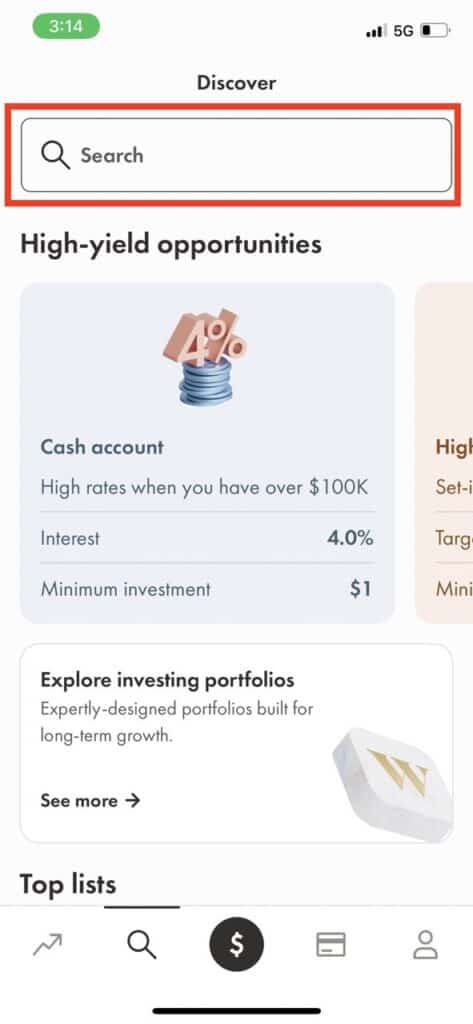

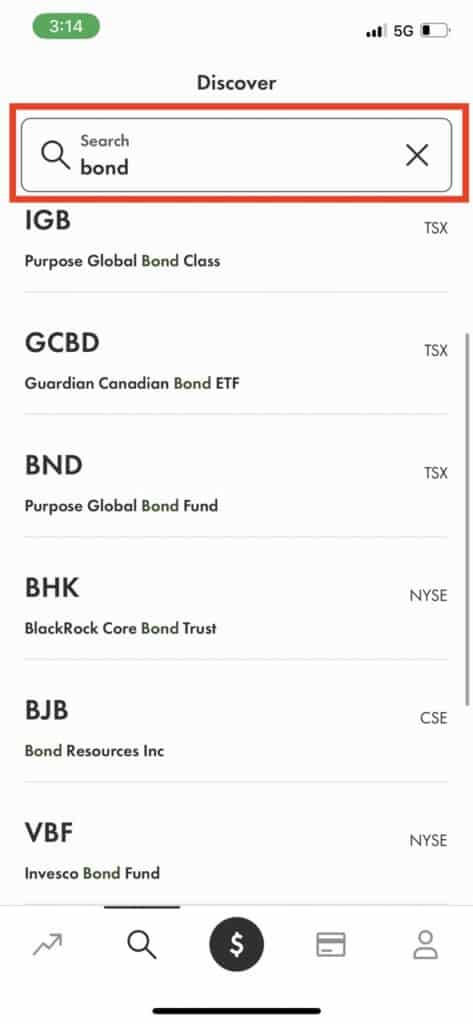

So if you want some exposure to the bond market and you have a Wealthsimple Trade account, all you would do is open up your account and then search for “bond” in the search bar.

You’ll then see a list of bond ETFs that you can easily go in and buy.

In the images below, you’ll see the steps I’d take to buy a Blackrock bond ETF [2].

So as you can see, it’s really straightforward. You can also search for “fixed income,” and you’ll see a lot more ETFs that contain a broad of fixed-income assets like bonds.

Noel’s Take on Wealthsimple Trade

Due to its low costs, diverse investment options and overall ease of use, I think Wealthsimple Trade is Canada’s best self-directed online brokerage platform, and I would give it a score of 4.5/5.

Buying Bond ETFs on Wealthsimple Invest

I just showed you how you can directly buy bond ETFs on Wealthsimple Trade. But Wealthsimple also has a robo-advisor investment platform where investors just set their risk level on a scale of 1-10 and let Wealthsimple do the rest.

Related Article by Noel: Wealthsimple Invest vs Trade 2023 | Which is Right For You?

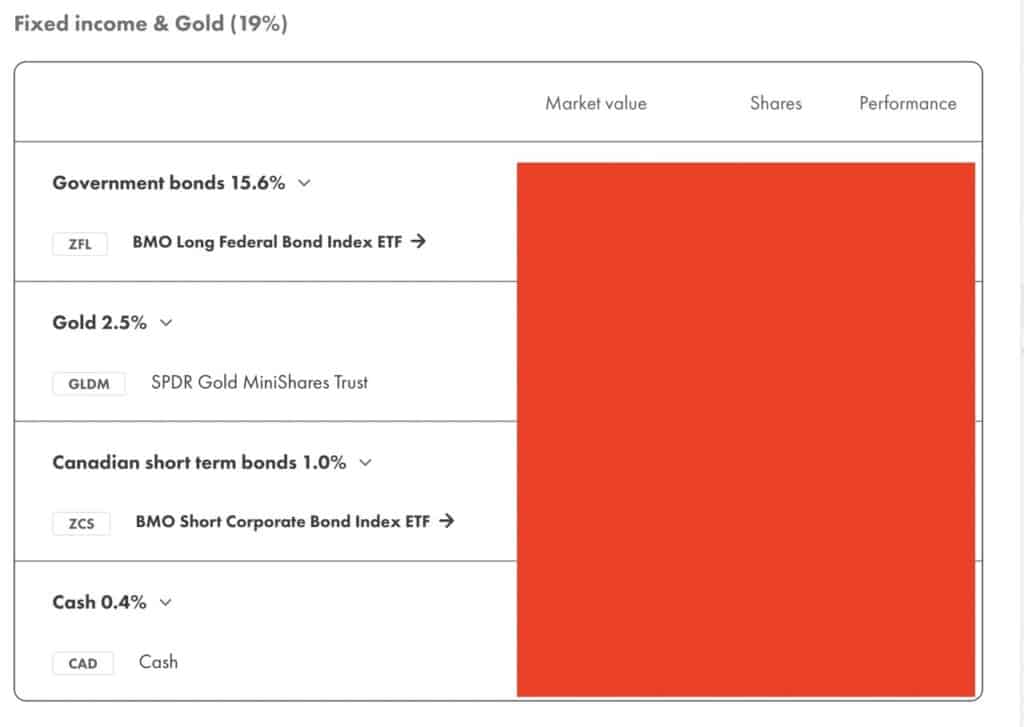

As you can see from my screenshot below, as part of my Wealthsimple Invest portfolio, Wealthsimple invests in some bond ETFs for me. About 19% of my Invest portfolio is in bonds, but again, the Invest platform is more of a “set-and-forget” investing approach.

Unlike Wealthsimple Trade, where I have to go in and research and buy the ETFs myself, Wealthsimple Invest does it all based on my risk level on a scale of 1-10. The riskier I want my portfolio to be, the less percentage of funds will be in bonds.

Check out my Wealthsimple Review article below for more details!

How to invest in bonds in Canada?

Okay, so now we know that we can indirectly buy bonds through Wealthsimple ETFs, but what about if you wanted to buy them directly?

How would one go about doing that?

Here’s a straightforward guide on how to buy bonds in Canada:

1. Understand What Bonds Are: To start, it’s important to grasp the concept of bonds. Essentially, a bond is a form of loan that you provide to a company or government. In exchange for the loan, the issuer pledges to pay you regular interest until the maturity date[3]. At that point, your initial investment (the principal) will be repaid

2. Familiarize Yourself with the Different Types of Bonds: There are a number of different types of bonds available for purchase in Canada, such as Government of Canada bonds, municipal bonds, high-yield or “junk” bonds, investment-grade corporate bonds, strip coupons, residual bonds, and provincial bonds.

So make sure you know what you investing in before so doing.

As the famous Dave Ramsey always says, ” don’t put your money into things you don’t know anything about”.

3. Choose a Platform or a Bank to Buy Bonds: You can buy bonds directly from brokers, financial institutions (like Questrade), or licensed financial advisors.

Canadian banks such as TD, Royal Bank, Scotiabank, CIBC, and BMO all offer bonds. The exact purchasing process might vary slightly across these platforms, but generally, you will need to create an investment account and select your preferred bonds or bond funds for the purchase.

And then of course, as outlined above, platforms like Wealthsimple are probably the easiest way to invest in bonds, as long as you are okay with owning them through a fund and not directly (that’s what I do).

The Bottom Line

So while direct bond purchasing isn’t an option on Wealthsimple in 2023, it looks like it is something that Wealthsimple has in its pipeline (according to Grace from Wealthsimple Customer Support)

So it’ll definitely be interesting to see when and if they roll that out.

But in the meantime, if investors don’t want to use another platform like Questrade or banks like RBC, then they can still gain exposure to the bond market through bond ETFs within the Wealthsimple platform. Whether you prefer the self-directed approach of Wealthsimple Trade or the automated ease of Wealthsimple Invest, both offer suitable pathways to include bonds within your investment portfolio.

FAQs

If you’re an investor in Canada looking for a balanced mix of equities and fixed income, bonds can be a great choice. They also help diversify your asset classes, especially if you mainly invest in stocks, ETFs, and mutual funds.

In the past, Canadian bonds have tended to perform better than GICs. Bloomberg reports that the FTSE Canada Universe Bond Index shows Canadian bonds have outperformed GICs about 80% of the time on a rolling one-year basis. When investors compare GICs with bonds, they typically only consider the current GIC rate and bond yield.