Wealthsimple RESP Review 2024: A Comprehensive Guide

Saving for your child’s education is a top priority for many parents, but navigating the world of education savings plans can be overwhelming.

That’s where Wealthsimple RESP comes in – a convenient, low-cost, and time-tested investment strategy designed to help parents save and invest for their children’s post-secondary education.

In this comprehensive Wealthsimple RESP review, we’ll explore the benefits, fees, and features of Wealthsimple RESP, and why it’s quickly becoming a top choice for many investors.

Key Takeaways

1. Reliable and Cost-Efficient

Opening a Wealthsimple RESP is a reliable and cost-efficient investment strategy for parents looking to save for their children’s post-secondary education.

2. User-Friendly

Wealthsimple offers competitive fees, a user-friendly platform, diverse portfolio options and the convenience of automatic rebalancing.

3. Safe and Secure

Wealthsimple RESP complies with stringent safety and regulatory standards providing additional protection to investors’ savings.

Introduction to Wealthsimple RESP

A Registered Education Savings Plan (RESP) [1] is a government-registered account intended to assist parents in saving and investing for their children’s post-secondary education, with the added benefit of tax advantages and government grants.

Parents have the option to contribute up to a lifetime maximum of $50,000 to each child’s RESP account, a crucial feature aiding in future education cost planning. In addition to the tax advantages and access to government grants, Wealthsimple RESPs are regulated by the Investment Industry Regulatory Organization of Canada (IIROC) [2], ensuring proper oversight and protection for investors.

Opening a Wealthsimple RESP brings the benefits of free government grants, straightforward investment strategies, and lower fees. Furthermore, your investments are protected by the Canadian Investor Protection Fund (CIPF)[3], providing an added layer of security by Wealthsimple for your hard-earned savings.

The Appeal of Wealthsimple RESP

One of the key appeals of a Wealthsimple RESP is its convenient, cost-efficient, and reliable investment strategy. With a Wealthsimple RESP, parents can benefit from:

Automated rebalancing

A selection of portfolio options to meet different risk thresholds and investment objectives

Easy investment in their children’s education without having to worry about managing their investments actively.

Wealthsimple RESPs offer competitive fees compared to other RESP providers. The fees for Wealthsimple Basic are as follows:

Annual fee: 0.5%

Foreign exchange conversion fee for investing in U.S. equities: 1.5%

ETF MERs (Management Expense Ratios): typically range from 0.10% to 0.20%

Adding account management fees often brings the total cost to between 0.50% and 0.70%, depending on the funds chosen. Compared to other RESP providers, Wealthsimple’s fees are relatively low, making it an attractive option for cost-conscious investors.

Beyond being a cost-effective solution, Wealthsimple RESP provides a plethora of investment options, catering to diverse risk tolerances and investment objectives. Through Wealthsimple’s robo advisor platform, investors can choose from:

Conservative portfolios

Balanced portfolios

Growth portfolios

Socially responsible investing (SRI) portfolios

Halal portfolios

This ensures diversification and alignment with investors’ values and objectives.

Opening a Wealthsimple RESP Account

Opening a Wealthsimple RESP account is a straightforward online process that typically takes less than 15 minutes. All you need to provide is your Social Insurance Number and that of your child(ren), as well as their respective names and dates of birth. Once your account is open, you may consider scheduling a financial planning session with a Wealthsimple advisor to discuss your investment goals and strategies.

Open a Wealthsimple RESP account through this exclusive link and receive a $25 bonus with an initial deposit of $500.

If you already have an RESP account with another financial institution, transferring it to Wealthsimple is also possible. Wealthsimple will cover the transfer fees up to $150 if the account value is above $5,000 [4], making it a seamless and cost-effective process for parents looking to consolidate their investments under one platform.

Exploring Wealthsimple RESP Account Types

Wealthsimple offers a range of RESP accounts. These include Individual and Family RESPs. Individual RESPs are designed to help families save for a single child’s post-secondary education expenses, and anyone related to the child, such as grandparents, uncles, aunts, and family friends, is eligible to open an individual RESP account on their behalf.

On the other hand, a Family RESP can be used for multiple children and is intended to provide more flexibility for families with more than one child. However, the subscriber must be a direct relative of the child to open a family RESP account. For example, a family RESP with three beneficiaries has a maximum contribution limit of $150,000 without penalty.

The decision between an Individual RESP and a Family RESP hinges on your family’s unique circumstances and investment objectives. Each account type has distinct contribution limits and grant eligibility, necessitating a thorough evaluation of which option aligns best with your needs and situation.

Diverse Portfolio Options in Wealthsimple RESP

As mentioned earlier, with a Wealthsimple RESP, you get an extensive array of portfolio options, accommodating a variety of investment preferences and risk tolerances. These portfolios include:

Conservative

Balanced

Growth

Socially responsible investing (SRI)

Halal options

This ensures that investors have access to diverse investment choices that align with their values and objectives.

The portfolios (which are controlled by robo-advisors) are composed of various asset classes, including:

Canadian stocks

US stocks

Global min-vol stocks

Foreign stocks

Emerging market min-vol stocks

Canadian long-term government bonds

Canadian short-term corporate debt

Physical gold bars

This broad range of investment options allows investors to build a well-diversified portfolio designed to weather market fluctuations and provide long-term growth.

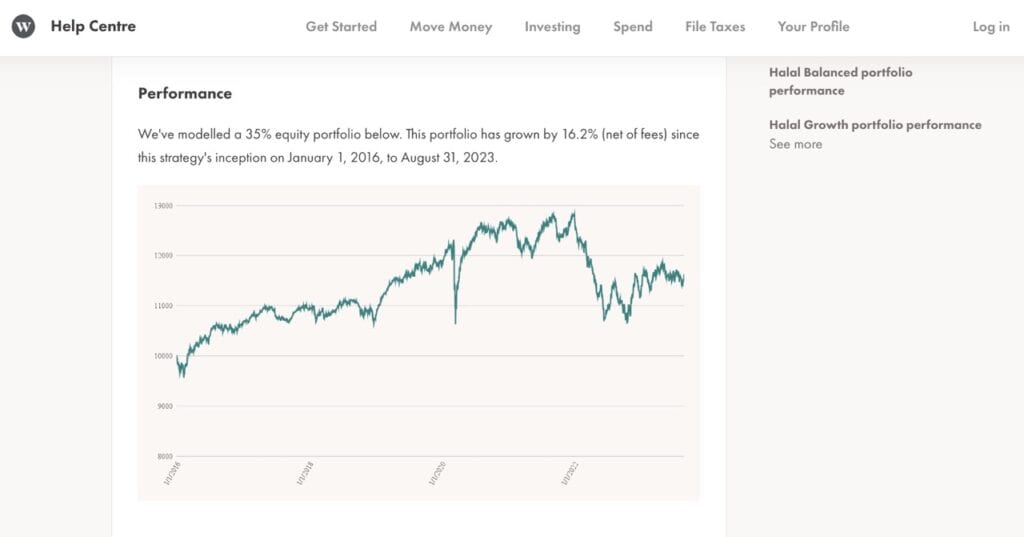

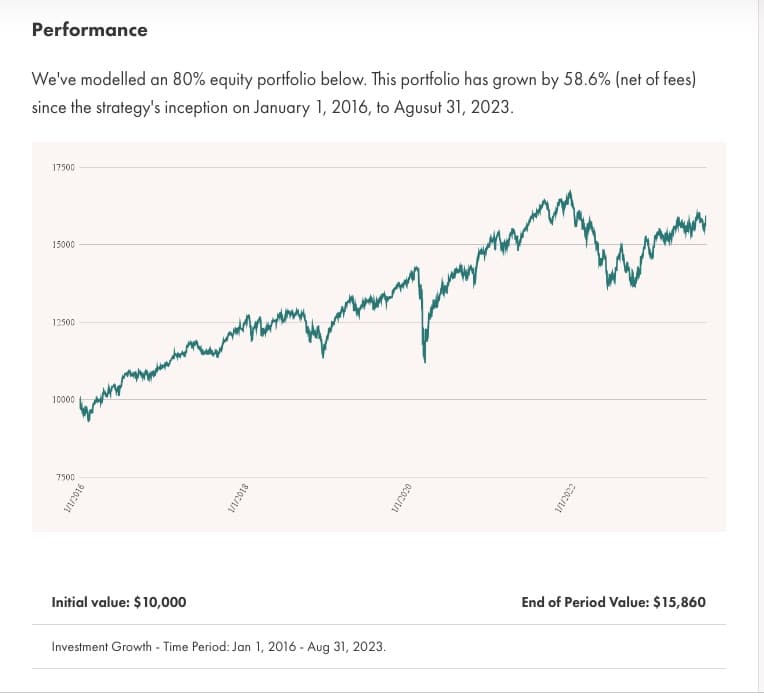

Wealthsimple RESP portfolios have demonstrated varying performance based on investment objectives – below are each of the portfolio types annualized returns since its 2014 inception.

Conservative portfolios (35% equity) achieved an annualized return of 2%

Balanced portfolios (50% equity) realized an annualized return of 3.11%

Growth portfolios (80% equity) achieved an annualized return of 5.64%

This range of performance showcases Wealthsimple RESP’s ability to cater to different investor goals and risk tolerances.

User-friendly Interface and Easy Transfers

Wealthsimple’s user-friendly platform enables convenient account management, expeditious transfers, and a unified experience with other Wealthsimple services, including the basic account. This ease of use allows investors to manage their Wealthsimple accounts, such as RESP accounts, with minimal effort, giving them more time to focus on other aspects of their personal finances.

As I touched on earlier, the process of transferring an existing RESP account or cash account from other financial institutions to Wealthsimple is smooth, with Wealthsimple absorbing the transfer fees for accounts valued at over $5,000. This ensures that investors can consolidate their investments under one platform without incurring additional costs.

And a quick note, whether you have your funds in an RESP or another account type – if you start using Wealthsimple and you realize it’s not for you, well withdrawing funds from a Wealthsimple account is also super super simple.

Here’s how:

Transfer funds to your linked Canadian bank account.

Note that funds must be held in the Wealthsimple account for five business days before withdrawal is possible.

Transfer processing can take up to seven days.

Assessing Wealthsimple RESP Performance

While assessing the performance of Wealthsimple RESP portfolios, it’s vital to take into account your risk tolerance and investment objectives. The portfolios have shown varying performance based on these factors, emphasizing the importance of long-term growth and risk management.

As I talk about in my Wealthsimple Review article, Wealthsimple users a slider that allows users to very easily adjust their risk level on a scale of 1-10. The higher the number you set, you’re telling Wealthsimple the more risk you’re willing to take on.

To review historical performance, investors can analyze the portfolio’s performance over time at these links:

This allows you to gain insight into how your investments would have fared in the past and make informed decisions about your future investment strategies. Additionally, performance can be compared to benchmark indices, providing a clear picture of how the portfolio is performing relative to the broader market.

While past performance is not indicative of future results, it’s highly recommended to consult with a financial advisor to ensure that your investment objectives are being met. This can help you make informed decisions about your Wealthsimple RESP account and optimize your investment strategy for your child’s future education expenses.

Safety Measures and Regulations

As I briefly mentioned earlier, Wealthsimple RESPs operate under IIROC and CIPF regulations, providing a secure environment for investors. The Investment Industry Regulatory Organization of Canada (IIROC) oversees the activities of investment dealers, while the Canadian Investor Protection Fund (CIPF) provides coverage for customer accounts in the event of Wealthsimple’s insolvency.

Related Article by Noel: Is Wealthsimple Safe? A Complete Overview for New Investors

It is important to remember that Wealthsimple does not guarantee the principal of your investments. Furthermore, investments in Wealthsimple RESP accounts are not insured by the CDIC (Canada Deposit Insurance Corporation). This means that investment values can still fluctuate based on market performance, so it’s essential to understand the inherent risks associated with investing in an RESP account.

Is a Wealthsimple RESP Worth It?

Considering the advantages and features that a Wealthsimple RESP offers, it’s clear that this platform is a valuable option for parents looking to invest in their children’s education. The convenience of its user-friendly interface, the diversification and performance offered by its portfolio options, and the competitive fees make Wealthsimple RESP an attractive choice for many investors.

While no investment option can guarantee returns, Wealthsimple RESP’s focus on long-term growth and risk management offers investors a solid foundation for building their children’s education savings.

Additionally, the platform’s adherence to strict safety measures and regulations ensures that investors can have peace of mind knowing that their Wealthsimple investments are protected.

In conclusion, Wealthsimple RESPs are a top choice for many investors seeking a convenient, low-cost, and time-tested investment strategy to help fund their children’s post-secondary education. Its diverse portfolio options, user-friendly platform, and competitive fees make it an appealing choice for parents looking to secure their children’s future. For more information, you can read my in-depth Wealthsimple review here.

Frequently Asked Questions

How trustworthy is Wealthsimple?

Wealthsimple is highly trustworthy, with over 1.5 million users across Canada and industry-standard security measures in place. Funds deposited into an account are held by CDIC members and are protected up to $300,000 in the aggregate, making it a safe option to save your money.

What is the maximum contribution limit for a Wealthsimple RESP account?

The maximum contribution limit for a Wealthsimple RESP account is $50,000 per child.