Wealthsimple TFSA Review for 2024 (Canada’s Best TFSA)

Key Takeaways

1. Tax-Free Benefits

With a Wealthsimple TFSA, investors benefit from tax-free investment income, allowing growth without taxation on returns.2. User-Centric Platform

Wealthsimple offers a user-friendly online setup process, easy withdrawals, and a well-designed mobile app, ensuring even beginners find it intuitive.3. Transparent Fees

The fee structure is clear and is based on the amount of money you have invested with Wealthsimple.4. Safety and Security

Regulated by IIROC with robust security, comparable to top Canadian banks – Wealthsimple ensures user data and investments remain secure.5. Portfolio Options

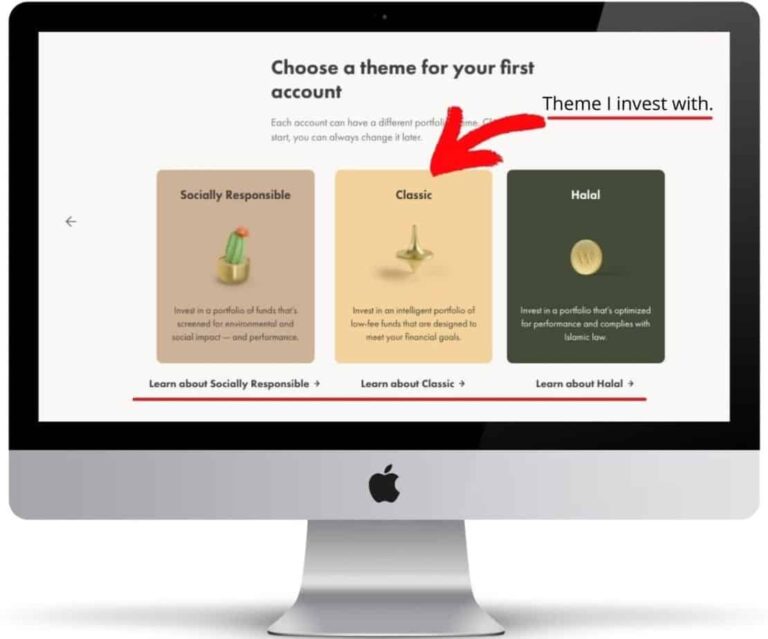

Apart from its straightforward investment process, Wealthsimple offers specialized themes for investment, such as Socially Responsible and Halal.

Main Pros and Cons of Wealthsimple TFSA

- Tax-Free investment income

- No account minimums

- Wealthsimple invests your money for you

- Low management fees (.5%)

- Mobile Friendly

- Contributions are not Tax Deductible

- Dividend Tax on Foreign Investment

- Wealthsimple Doesn’t Offer 24/7 Support

- Competitive Fees

- Day Trading is Not Allowed

What is a Wealthsimple TFSA?

Similar to a Wealthsimple RRSP, Wealthsimple TFSAs are registered investment accounts.

A TFSA differs from an RRSP as TFSA contributions aren’t tax-deductible, but they do allow for tax-free withdrawals. So, for example, if you invested $1,000 in a tax-free savings account in 2023 and then that turned into $2,000 by 2024, well, you wouldn’t have to pay taxes on that income – hence the tax-free.

So when we refer to a Wealthsimple TFSA, the TFSA part is something that was actually created by the Canadian government [1], and Wealthsimple comes in as the TFSA issuer – the place where Canadians can come and sign for an investment account and invest within it.

Having been with Wealthsimple since early 2018 (when I transitioned my Scotiabank TFSA over to a Wealthsimple TFSA), I can vouch for Wealthsimple and its excellence as a platform. This article will delve deeper into my experience and the platform’s merits.

Important Note

Wealthsimple Invest is Wealthsimple’s automated investment product and is a much more hands-off style of investing, which most people love. But if you’re someone who wants to manage your entire portfolio yourself by buying and selling individual stocks (or ETFs), then you should set up an account with Wealthsimple’s direct investing platform, Wealthsimple Trade.

Learn More about Wealthsimple Trade and How It Differs From Wealthsimple Invest.

Wealthsimple TFSA Review | Pros and Cons

Before exploring the advantages and drawbacks of Wealthsimple TFSA account types, it’s essential to distinguish between elements stemming from Wealthsimple’s role as an issuer and the unique attributes of the TFSA account type.

A case in point: TFSA deposits not being tax-deductible is not a lapse on Wealthsimple’s part.

Pros

Cons

Does Wealthsimple Charge Fees For TFSAs?

Wealthsimple Invest has carved a niche for itself with its intuitive, user-centric platform. But like any financial institution, one of the ways it generates its income is from a specific fee structure. If you’re considering or already have a TFSA with Wealthsimple Invest, it’s vital to understand these fees.

Remember: We are referring to the Wealthsimple Invest platform here, which is Wealtthsimple’s robo advisor, if you’re interested in the fee structure for their direct investing platform – Wealthsimple Trade, check out my article here.

Fee Structure For Wealthsimple Invest TFSA

The fees you encounter on Wealthsimple Invest depend on your investment amount. There are three primary minimum investment tiers:

- Core

- Premium

- Generation

Here’s a snapshot of the management fees for each:

| Plan | Amount Invested in Your TFSA | Management Charge |

|---|---|---|

| Core | Starting at $1 – $99,999 | 0.5% |

| Premium | $100,000 – $499,999 | 0.4% |

| Generation | $500,000 | 0.2% – 0.4% |

Understanding Wealthsimple Fees With Examples

- Core Tier: On an investment of $50,000, you’d pay:

- $50,000 x 0.5% = $250 annually, or about $20.83 each month.

- Premium Tier: For an investment of $150,000, you’d be charged:

- $150,000 x 0.4% = $600 annually, or roughly $50 monthly.

- Generation Tier: With a $1,000,000 investment at 0.3%, your fee is:

- $1,000,000 x 0.3% = $3,000 annually, or $250 each month.

These charges are conveniently deducted from your account.

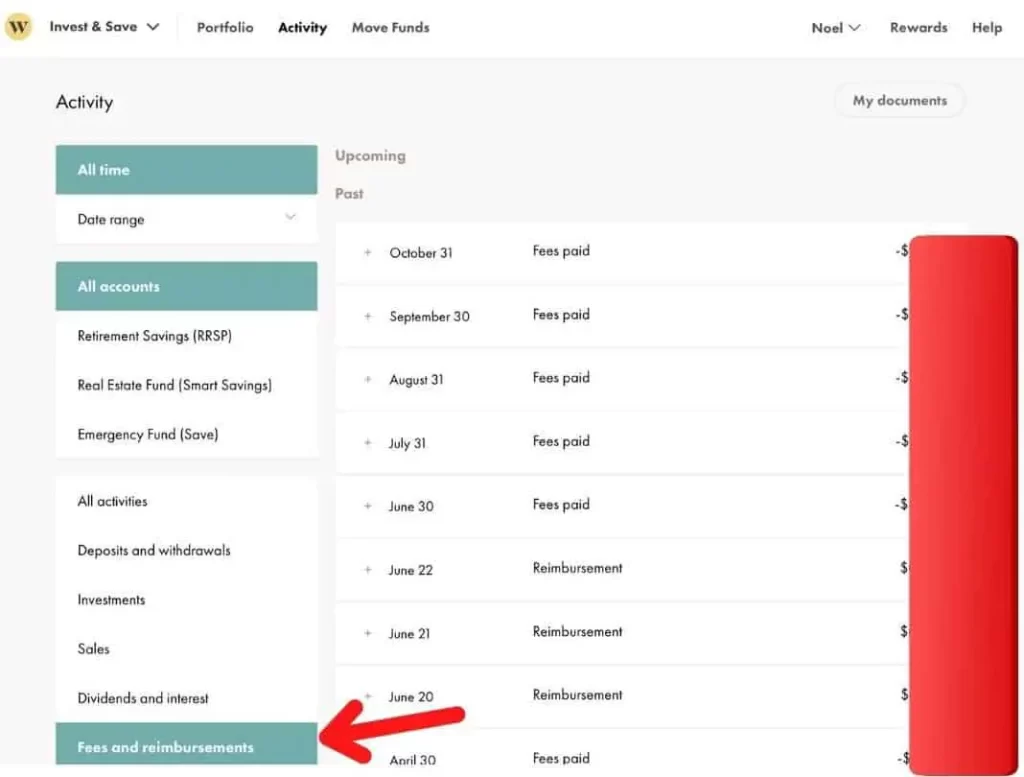

Monitoring Your Fees

To track the account fees within Wealthsimple Invest, navigate to the “Activity” tab. Then choose the account type (in this case, TFSA) and then select “fees and reimbursements”.

This provides a transparent view of management fees and all charges, keeping you updated on your investment’s management fees and expenses.

How to Open a Wealthsimple TFSA

Time needed: 20 minutes

Embarking on your investment journey with a TFSA on Wealthsimple Invest is a seamless experience. Follow this streamlined guide, and you’ll quickly transition from a newbie to an investor.

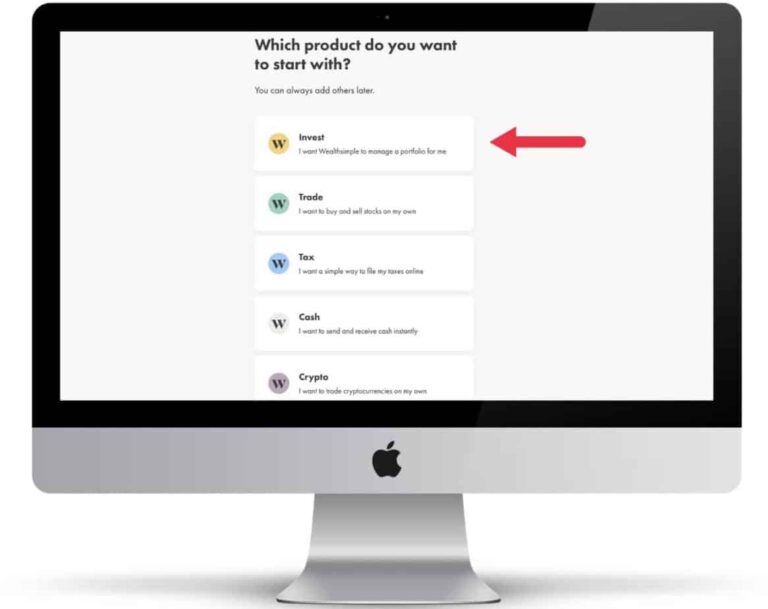

- Create a Wealthsimple Profile

Initiate by navigating to the Wealthsimple sign-up portal and begin your profile creation using your email address and selecting a password.

Choose “Invest” as your primary product.

Then you’ll be asked to provide the following details:

1. First Name

2. Last Name

3. Date of Birth

4. Phone Number

5. Citizenship

6. Gender (Optional)

7. Residential Address

8. Mailing Address

9. Employment Status

10. Current Workplace

11. Type of Company

12. Your Role at the Company

13. Social Insurance Number (SIN)

Rest assured, your information is in safe hands. Wealthsimple operates under the stringent regulations set by IIROC (Investment Industry Regulatory Organization [2]), mirroring the security measures of prominent Canadian banks.

Related Article: Is Wealthsimple Safe? A Complete Overview for New Investors - Personalize Your Portfolio

Next, you’ll engage with a questionnaire designed to curate an investment strategy tailored to your ambitions and risk appetite.

Your responses to the following inquiries help in this customization:

1. Are you thinking about retirement?

2. What’s the main reason for investing?

3. When would you like to retire?

4. What’s your estimated household income for this year?

5. How much money do you have saved?

6. What’s the value of property and other assets you own?

7. What’s the value of your debts?

8. How much do you know about investing?

9. Do you have an idea of how much risk you’re willing to take?

10. Choose an investment theme for your account (Socially Responsible, Classic, Halal)

After completing this, Wealthsimple will propose a portfolio they think best suits your needs. However, you possess complete autonomy here—you can fine-tune your risk parameters after you finish registration. - Open Your Wealthsimple Account

Now, it’s time to lay the foundation of your account.

Decide at the outset if you’re transferring over an existing investment or starting a new one.

If you’re starting a new account, you should opt for “No, I’ll start with a new Wealthsimple account.”

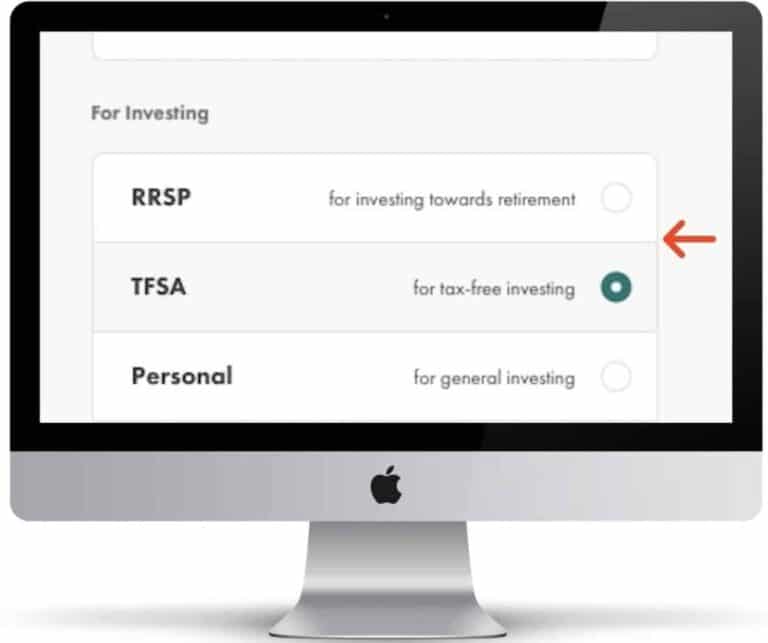

Select the account that aligns with your objectives., which in this case will be the TFSA and then finalize your objectives, review, and accept the terms.

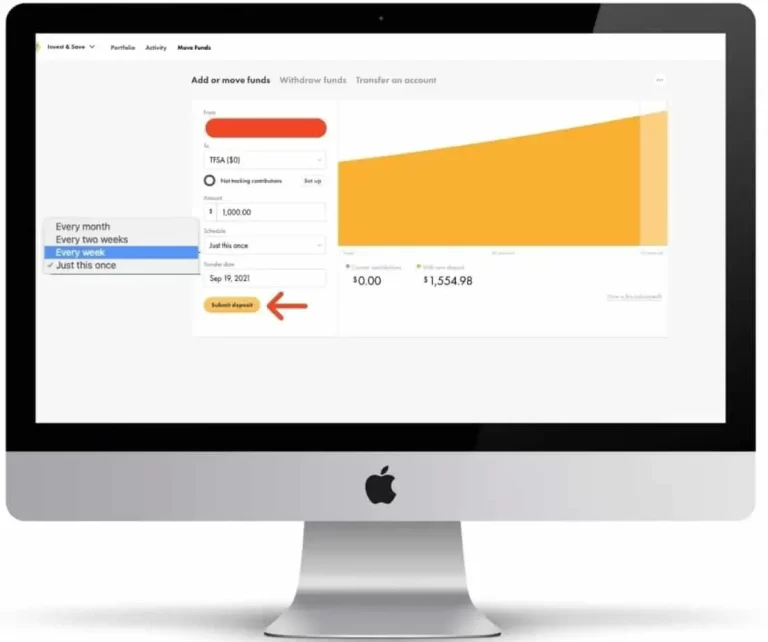

- Fund Your Wealthsimple TFSA

You’ll now link your bank account to Wealthsimple and fund your investment account. Connecting your bank to Wealthsimple is safe, and the platform connects to all credible banks in Canada.

Once you’ve linked your bank account, you’ll schedule a deposit by following these steps:

1. Ente the amount you want deposited

2. Schedule the deposit for a one-time transaction or weekly, bi-weekly, or monthly

3. Select the deposit date

Now click “Submit deposit.” It can take anywhere from 3-5 business days for deposits to be complete and deposited into your account.

You’ve officially set up and funded a TFSA with Wealthsimple.

Final Verdict

Based on my experience, Wealthsimple’s TFSA earns a strong 4.5 out of 5-star rating from me.

If you’re on the fence about joining, remember it’s risk-free to test the waters. If it aligns with your needs, fantastic! Otherwise, you can effortlessly close your account in under a minute without any fees. Either way, you’ll have clarity on its fit for you.

FAQs About Wealthsimple

What Are The Downsides of a Wealthsimple Account?

One of the downsides of the Wealthsimple portfolio’s basic account services is that it comes with higher investment fees (0.5%) in comparison to its premium offerings (0.2% – 0.4%).

Is It Safe To Invest Through Wealthsimple?

Wealthsimple is a safe, socially responsible investing platform to invest your money in. Not only does it have 1.5 million users and over $15 billion in assets under management, but Wealthsimple has also gained a great reputation in Canada for being an overall safe, legitimate and socially responsible investing platform.[3]

Are There Hidden Fees With Wealthsimple?

Wealthsimple doesn’t burden its users with commission fees, transfer fees, costs, or any other hidden fees.

Is It A Good Idea To Open A TFSA With Wealthsimple?

Deciding to open a TFSA could be very beneficial for you if you have financial objectives that might necessitate withdrawing funds before you hit retirement. Even if you’re targeting retirement, a TFSA might still be a great option for you to save money, especially if your yearly earnings are under $50,000.

How Does a Wealthsimple Invest Account Differ from a Wealthsimple Trade Account?

Wealthsimple Invest serves as Wealthsimple’s robo-advisor platform, offering managed investment solutions. On the other hand, the Wealthsimple Trade app empowers investors with a DIY trading platform, allowing them to handpick stocks and ETFs for their portfolios.

What is Wealthsimple Cash?

Wealthsimple Cash is a product offered by Wealthsimple, designed primarily as a cash account for easy money management and spending. It provides users with the convenience of holding and accessing cash, similar to a traditional bank account. Notably, assets held in Wealthsimple Cash are protected under the Canadian Investor Protection Fund[4], ensuring added security for users.

![Can You Buy Gold on Wealthsimple? [January 2024 Update]](https://noelmoffatt.com/wp-content/uploads/2023/08/Can-You-Buy-Gold-on-Wealthsimple-2.jpeg)

![How to Withdraw Money from Wealthsimple [with Screenshots]](https://noelmoffatt.com/wp-content/uploads/2023/07/How-to-Withdraw-Money-from-Wealthsimple-768x327.jpg)

![How To Buy Dividend Stocks On Wealthsimple [2024 Tutorial]](https://noelmoffatt.com/wp-content/uploads/2023/08/How-tp-Buy-Dividend-Stocks-on-Wealthsimple-768x538.jpg)