Wealthsimple TFSA vs Personal Account | Simple Comparison

If You’re In a Rush

Wealthsimple TFSA vs Personal Account

Any investment income generated in a Wealthsimple TFSA will be tax-free, while any income generated within your Wealthsimple personal account will be taxed by the Canadian government.

This article will explore the key differences between a Tax-Free Savings Account (TFSA) and a Personal Account on Wealthsimple. Wealthsimple, a popular online investment platform, offers a wide range of investment options for both beginners and experienced investors.

Whether you’re new to investing or looking to continue to grow your wealth, understanding the differences between these account types can help you make better-informed decisions.

In short, the main difference between a TFSA and a personal account on Wealthsimple is the tax implications that occur on any income you generate within your account. Any income generated in a TFSA will be tax-free, while any income generated within your personal account will be taxable by the Canadian government.

Compared At a Glance

| Comparison | Wealthsimple Personal | Wealthsimple TFSA |

|---|---|---|

| Tax on Investment Profits | Taxable | Tax-Free |

| Tax Deduction on Losses | Possible | Not Allowed |

| Limit on Deposits | No Limit | Limited to TFSA Contribution Limit[1] |

| Day Trading Rules | Allowed (No Limit on Trades) | May Be Penalized to Taxed |

| Cash Withdrawals | Allowed at Any Time | Allowed at Any Time |

Now let’s dive into the details of each account type, starting with an overview of how they differ, then a closer examination of their individual characteristics and a guide to choosing the one that best fits your investment goals.

TFSA vs Personal Account on Wealthsimple | How They Differ

Okay, now that we know the basics of how a TFSA and a personal account differ, it’s time to take a closer look at each account type.

What is a TFSA on Wealthsimple?

A TFSA on Wealthsimple is a registered investment account that allows Canadians to invest in assets such as stocks and ETFs while generating tax-free investment income.

In other words, if you open a TFSA with Wealthsimple and invest $1,000 into Apple’s stock[2] and you make $100 over the course of a few months – now, the value of your Apple stock is $1,100. If you decided to take your profit of $100, you could sell and withdraw that $100 completely tax-free because it is your tax-free savings account.

An important note: The rules associated with a “Wealthsimple TFSA” are no different than any other TFSA with another financial institution. For example, if you opened up a TFSA with Questrade, all the same tax rules would apply.

What is a Personal Account on Wealthsimple?

A Personal Account on Wealthsimple differs from a TFSA as any investment income generated in a personal account is subject to taxes. Additionally, losses are tax deductible, and there’s no limit to the amount you can deposit in your personal account.

I personally only have a TFSA opened up with my Wealthsimple Trade account right now – as I haven’t yet capped out my contribution limit, it wouldn’t really make sense for me to invest in a taxable account until my TFSA contribution room is maxed out.

Wealthsimple TFSA vs Personal Account: Main Difference Summarized

So as you can probably tell – the primary distinctions between Wealthsimple Personal and Wealthsimple TFSA accounts revolve around taxation, trading limits, and deposit constraints.

Wealthsimple Personal Accounts permit unlimited deposits and trades and allow for tax deductions on losses, but any actual cash gains from stock investments are taxable. On the other hand, a Wealthsimple TFSA offers tax-free gains but is restricted by the amount you can deposit (by the CRA) – also known as your TFSA Contribution Limit, losses are also not deductible, and day trading may be penalized to taxed d by the CRA [3] .

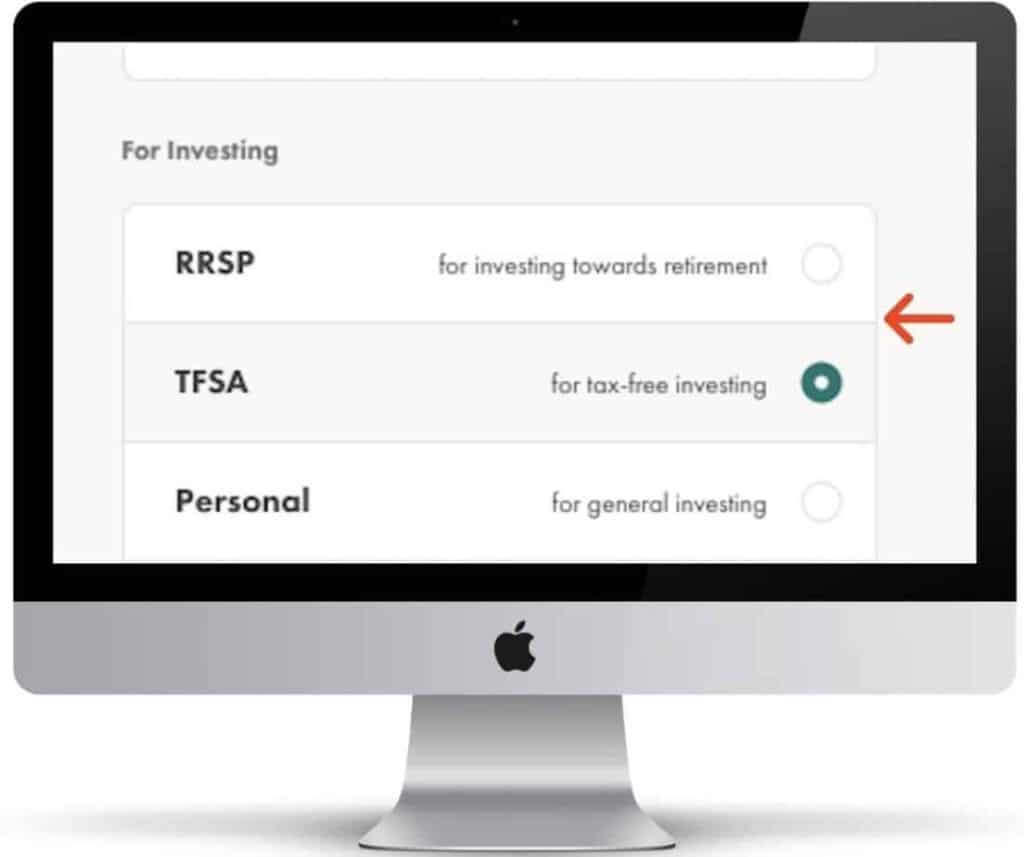

Step 1 – If you haven’t already, register for your CRA online account.

Step 2 – Login to your CRA online account

Step 3 – Scroll down to the bottom of your homepage.

Step 4 – Look at the amount assigned to your “TFSA Contribution Room”.

Step 5- Using a calculator, subtract all your TFSA deposits, since January 1st of the current year, from your TFSA Contribution Room.

Step 6- This value is your TFSA contribution limit as of today.

Your current TFSA limit is the amount you’re left with after subtracting current year’s deposits from your Contribution Room given to you by the CRA.

In other words, this is how much more you can contribute in your TFSA until December 31st.

One thing these accounts do have in common is that they offer the flexibility of cash withdrawals at any time without any penalties or restrictions.

What Type of Account Should You Open on Wealthsimple?

If you’re still deciding on which type of account you should open and you’re not quite sure if a TFSA or personal account makes sense for you, this next section might help.

You Should Open Up a TFSA with Wealthsimple if…

- You Want Tax-Free Gains: You seek to grow your investments without incurring taxes on the gains, capitalizing on the tax-free benefits.

- You Have Not Maxed Out Your Contribution Limit: Your TFSA contribution room is not yet filled, making investing in this account advantageous.

- You Invest in Mainstream Assets: You are primarily interested in investing in common stocks and ETFs without the complexity of day trading.

- You Are a Canadian Citizen or Resident: You meet the eligibility requirements and want an investment account tailored to Canadian tax laws.

- You Prefer a Restricted, Regulated Approach: You value the structured limitations on deposit.

You Should Open Up a Personal Account with Wealthsimple if…

- You Want Flexibility with Deposits: You desire the ability to deposit unlimited funds without the constraints of a contribution limit.

- You Seek Tax Deductions on Losses: You want the option to potentially write off investment losses against other taxable income.

- You Are an Active Trader: You wish to engage in frequent or day trading without the limitations or penalties that may apply to a TFSA.

- You Have Maxed Out Your TFSA Contribution Room: You’ve already reached your TFSA limit and need an alternative account to continue investing.

- You Desire More Investment Options: You seek a broader range of investment opportunities that may not be suitable or permitted within a TFSA.

Now regardless of what type of account you open, it’s important to note that the functionality and user experience of the Wealthsimple platform will be the same. The sign-up process, the features, how it works – everything is the same, the only difference between these accounts is how they’re regulated by the government.

Should I Open My Account with Wealthsimple Invest Or Trade?

When it comes to deciding between Wealthsimple Invest and Trade, that’s pretty straightforward – if you want a hands-off approach to investing and you just want to let Wealthsimple do all the investing for you, open up a Wealthsimple Invest account.

Wealthsimple Invest Pros and Cons

Pros

Cons

If you want to actively invest in stocks and ETFs yourself, then open a Wealthsimple Trade account. In other words, if you want to personally go into your account and purchase an Apple or Tesla stock, then you’d do this on the Wealthsimple Trade platform.

Wealthsimple Trade Pros and Cons

Pros

Cons

And then, when you’re signing up for your account, whether you choose Invest or Trade, you’ll be given the option, as you’ll see below, to select either a TFSA or Personal.

So here’s how I would approach it – if you don’t already have a TFSA, open up a TFSA with Wealthsimple over a personal account because you’ll get tax breaks, as I discussed throughout the article.

If you already have a TFSA maxed out with Wealthsimple, open a personal account.

The Bottom Line

Deciding between Wealthsimple’s TFSA and Personal Account really just boils down to your individual financial situation, investment goals, and preferences.

If tax-free gains and regulated deposit constraints align with your financial plan, the TFSA might be your ideal choice. Alternatively, if you seeking more flexibility in your deposits, potential tax deductions on losses, or you’ve maxed out your TFSA contribution room, a Personal Account is probably a better option.

And at the end of the day, both accounts offer unique advantages, so the right choice will hinge on understanding your own investment landscape and what you personally prioritize most in your investment journey.

If you’re new to investing or unsure about your specific needs, I’d suggest seeking professional financial guidance that can further assist in making the best decision for you.

FAQs about Wealthsimple Accounts

Yes, if you are saving and investing for goals that could require e a withdrawal prior to retirement, a TFSA is an ideal option for you. Furthermore, even if you intend to utilize a TFSA for retirement savings, it can be an attractive choice thanks to its tax-free growth and withdrawal benefits.

If you open a TFSA with Wealthsimple Invest, you’ll be charged a management fee of 0.4% – 0.5%. On the other hand, if you open a Wealthsimple Trade account, while there are no commissions for buying and selling stocks, you will be charged a currency conversion fee of 1.5% – 2% per transaction. Check out my article here to learn more about Wealthsimple Trade’s fees.

The best type of account to open with Wealthsimple depends on your individual financial goals and needs. Whether you are looking for retirement savings through an RRSP, tax-free growth with a TFSA, or personalized investment portfolios, Wealthsimple offers various options tailored to different investment strategies. Consult with a financial advisor or explore Wealthsimple’s offerings to find the best fit for your financial situation.