Can You Buy GICs on Wealthsimple? [Here are the Facts]

If You’re In a Rush

Can You Buy GICs on Wealthsimple?

Wealthsimple is a popular online investment platform that offers a range of investment products. However, at this time, GICs are not available for purchase on Wealthsimple.

In today’s fast-paced world of investing, it’s important to know your options.

One question that often comes up is whether you can buy Guaranteed Investment Certificates (GICs[1]) on Canada’s popular investment platform, Wealthsimple.

In this article, we will explore the facts surrounding this question and then provide you with some GIC alternatives that can be used on Wealthsimple’s platform.

Can You Buy GICs on Wealthsimple?

Wealthsimple, a popular online investment platform, offers many investment products – however, at this time, GICs are unavailable for purchase on either Wealthsimple Invest or Trade.

While the platform does offer a variety of other investment options, such as stocks, ETFs, crypto, tax services, robo advising, and so much more – GICs are not currently part of their product lineup.

If you’re specifically looking to invest in GICs, you’ll need to explore alternative options outside of Wealthsimple, which we will get into later. But for now, just know that you cannot buy GICs on Wealthsimple.

With that being said, though, – as I explain in the next section – Wealthsimple does offer other products and workarounds that function very similarly to a GIC, which could be something you consider.

GIC Alternatives on Wealthsimple

Okay, so now that we know GICs are not available on Wealthsimple, here are four ways you can use Wealthsimple’s products to invest your money that will give you similar outcomes as investing in GICs.

1. Buying Bond ETFs on Wealthsimple Trade

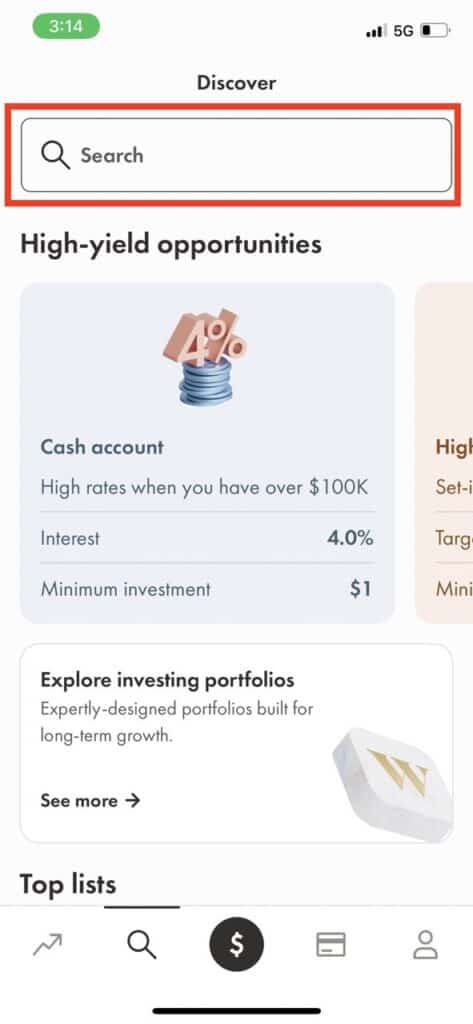

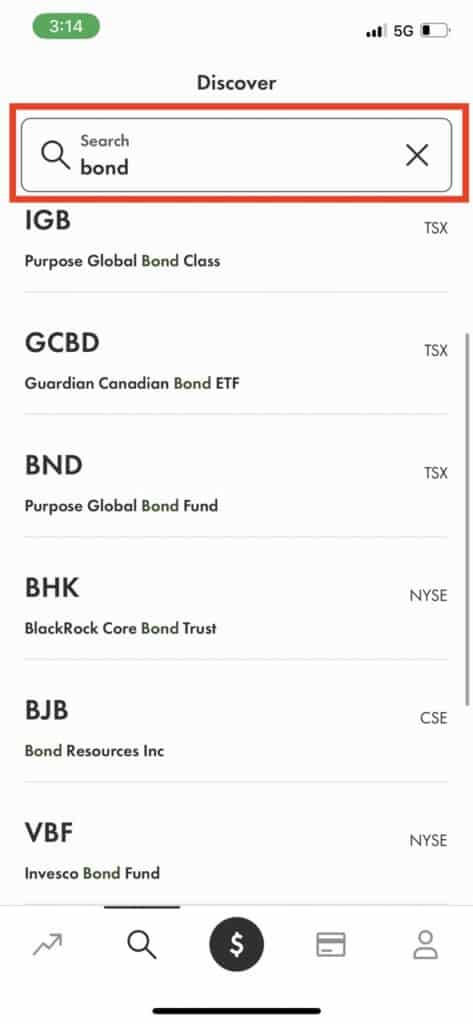

As you may know, Wealthsimple has a popular product called Wealthsimple Trade, which is Wealthsimple’s direct investing platform. And as I talk about in my article here, you can’t directly buy bonds on Wealthsimple Trade, but what you can do is buy bond ETFs – which is just a specific category of exchange-traded funds that solely invest in bonds.

As you can see from my screenshots below, it’s a pretty straightforward process once you have your Trade account open.

If you’re in the dark on bonds, they’re basically just a type of security in which the entity that issues the bond incurs a debt obligation to the bondholder. And then depending on the specific terms, the issuer is then required to cash flow to the creditor, as defined by the conditions of the bond.

All that to say, GICs and bonds are very similar in that they are very low in risk and often produce cash flow back to the creditor (which would be you). While bonds and bond ETFs still pose a risk[3], it’s going to be a lot lower than if you were to invest in an individual stock.

If going down the bond ETF route is something you think makes sense for you, you can get started with Wealthsimple Trade here.

Noel’s Take on Wealthsimple Trade

Due to its low costs, diverse investment options and overall ease of use, I think Wealthsimple Trade is Canada’s best self-directed online brokerage platform, and I would give it a score of 4.5/5.

2. Wealthsimple Savings Account

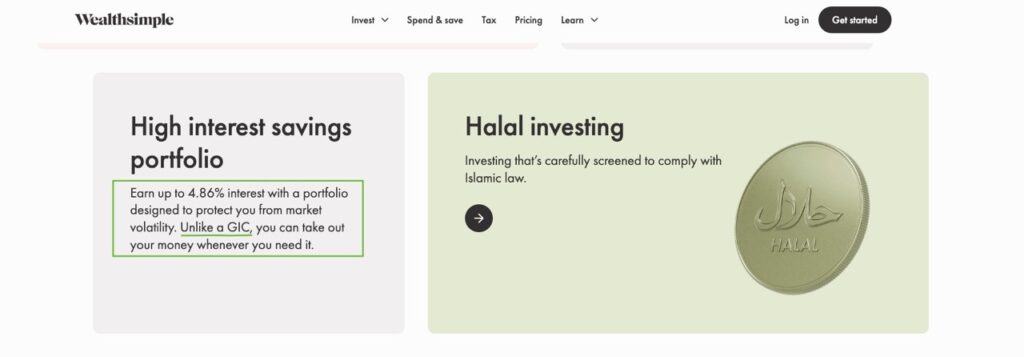

Within the Wealthsimple Invest product, Wealthsimple offers another high-interest savings account (which is separate from the one in Cash) that offers an interest rate of up to 4.86% [2], which, again, is a higher interest rate than the returns I see coming from GICs.

In fact, Wealthsimple even takes a little dig at GICs on their Wealthsimple Invest landing page, where they state, “Earn up to 4.86% interest with a portfolio designed to protect you from market volatility. Unlike a GIC, you can take out your money whenever you need it.”

I think this is another really good option for Canadian investors – I personally use this high-interest savings account on Wealthsimple Invest for my emergency fund, and it works great while I collect on absurdly high-interest rates each month.

3. Low Risk Wealthsimple Invest Account

Another option within Wealthsimple Invest is to set up an investment account with their robo-advisor and set your risk level to very low.

For those who don’t know, Wealthsimple’s robo-advisor is their original (OG) product. I’ve used it since 2018 for my RRSP and still to this day really enjoy it and think its a great product. What makes it great is its hand-off approach. You just deposit your money, set your risk level on a scale of 1-10 and then let them do the rest.

As you can see from my video below, setting your risk level is quite straightforward….to say the least.

If you’re looking to invest in GICs, you’re probably looking for very low-risk investments, which means you should put your risk level somewhere between 1-5.

So now we know there are two different ways you can use Wealthsimple Invest to put your money somewhere that will be safe while still providing you with a tidy little return. For a full overview of Wealthsimple Invest, my review article here of Wealthsimple Invest breaks down everything you need to know.

Wealthsimple Invest Quick Review

1. Robo Advisor

Wealthsimple Invest, the focus of this review, is Wealthsimple’s robo advisor, which caters to investors who prefer a hands-off approach to their investment strategy.2. Beginner-Friendly

Designed for beginner investors with a user-friendly interface on both desktop and mobile and a simple account setup process.3. Transparency

Transparent and straightforward fee structure, with no minimum deposit and clear information on both fees and returns.4. Account Options

Offers various account types, including personal accounts, TFSA, RRSP, and various investment options to suit investor risk levels and goals.5. Reputation for Safety

Wealthsimple has a well-established reputation for being safe and secure, with robust security measures and regulatory compliance.

4. Wealthsimple Cash Account

Wealthsimple has a product called “Wealthsimple Cash” traditionally, but I believe some people refer to it as “Wealthsimple Spend” now – but regardless of its name, it’s a cash account that acts as a hybrid between a chequing account and a high-interest savings account.

What’s even better? The interest rates on these accounts are wild – they start at 4%, and as your net deposits grow, your interest rates also climb. The table below shows the various interest rates offered by Wealthsimple based on the client type and the associated deposit requirements.

| Client Type | Interest Rate | Net Deposit Requirements |

|---|---|---|

| Core Client | 4% | No minimum balance |

| Premium Client | 4.5% | $100,000 in deposits |

| Generation Client | 5% | $500,000 in deposits |

So as you can tell, these interest rate numbers are pretty impressive and would actually outperform most GICs while still maintaining extremely low risk.

If you want to learn more, check out my in-depth review of Wealthsimple Cash.

Noel’s Take on Wealthsimple Cash

I give Wealthsimple Cash a solid 4.5/5 rating. It’s super easy to use, gives cash back on all spending, always innovates and releases cool features, and its potential to curb overspending makes it a worthy tool in my financial toolbox.

The Bottom Line

Although Guaranteed Investment Certificates (GICs) are not available on Wealthsimple, the platform still presents numerous alternatives for investors seeking low-risk options with promising returns – as outlined above.

From the Wealthsimple Cash Account, with interest rates that can outperform most GICs, to low-risk Wealthsimple Invest Accounts and bond ETFs on Wealthsimple Trade, there are several pathways for investments that act and perform very similarly to GICs. For those specifically interested in GIC-like products, the alternatives provided by Wealthsimple can achieve similar outcomes while sometimes even surpassing the traditional returns from GICs.

FAQ about GICs

iTRADE does, in fact, provide the option for self-directed investors to buy an extensive array of investments, including equities (Stocks and ETFs) and fixed-income (bonds and GIC), as well as options.

Yes, you can invest in a Guaranteed Investment Certificate (GIC) within a Tax-Free Savings Account (TFSA). Many financial institutions offer this option, allowing tax-free growth of the investment.

The main concern with GICs is the possibility of capital erosion, where the interest rate of your GIC could fall short of the prevailing inflation rate. For example, if you were to invest $10,000 in a 1-year GIC at an interest rate of 2%, and inflation ran at 3% during that period, then you would actually be losing purchasing power.

![How To Buy Dividend Stocks On Wealthsimple [2024 Tutorial]](https://noelmoffatt.com/wp-content/uploads/2023/08/How-tp-Buy-Dividend-Stocks-on-Wealthsimple-768x538.jpg)